After a major storm hits Monmouth County, homeowners face two parallel challenges: stopping the damage from getting worse and navigating the insurance claim process. The average water damage repair cost after Hurricane Sandy topped $38,000 per property, and even routine winter storms can cause $5,000–$15,000 in damage from ice dams, fallen branches, and frozen pipes.

Knowing what your homeowner’s insurance covers, what documentation you need, and when a handyman is the right call vs. a specialty contractor can save you thousands and prevent a denied claim.

Key Takeaways

- Homeowner’s insurance in NJ covers sudden and accidental water damage (burst pipes, storm-driven rain through the roof) but typically excludes gradual leaks and flood damage.

- After Hurricane Sandy, NJ homeowners filed over 55,000 flood insurance claims with average repair costs topping $38,000 per property.

- Filing a water damage claim starts with contacting your insurance company immediately, documenting all damage with photos and videos, and keeping every receipt for emergency repairs.

- A handyman handles the repair side, drywall replacement, painting, minor carpentry, gutter and siding fixes, while specialty contractors handle structural, roofing, and major plumbing work.

- Winter storms can cause major damage to NJ homes, including ice dams, frozen pipes, and roof collapse from snow load most of which is covered under standard homeowner’s policies.

What Homeowner’s Insurance Covers (and What It Doesn’t)

Understanding the difference between covered and excluded water damage is the single most important thing a NJ homeowner can know before a storm hits.

Typically Covered

- Burst pipes — sudden pipe failure from freezing is covered, including resulting water damage to walls, floors, and personal property

- Storm-driven rain entering through storm-damaged roof, windows, or siding — the resulting interior damage is covered

- Ice dam backup — water damage from ice dams that force water under roofing materials is generally covered if the ice dam resulted from a covered peril

- Appliance overflow — washing machine, dishwasher, or water heater failures that cause sudden flooding

- Wind damage — fallen trees, torn siding, missing shingles, and structural damage from high winds

Typically NOT Covered

- Gradual leaks — a slow pipe drip over months, seepage through the foundation, or a roof leak you’ve ignored for a season

- Flood damage — standing water from rising rivers, storm surge, or overflowing creeks requires a separate flood insurance policy

- Sewer backup — requires a specific rider endorsement on most standard policies

- Neglect and deferred maintenance — if the damage resulted from your failure to maintain the property, coverage may be denied

The critical distinction is sudden vs. gradual. A pipe that bursts at 2 AM and floods your basement is covered. A slow leak under your kitchen sink that’s been dripping for six months and rotted the cabinet isn’t.

The Insurance Claim Process — Step by Step

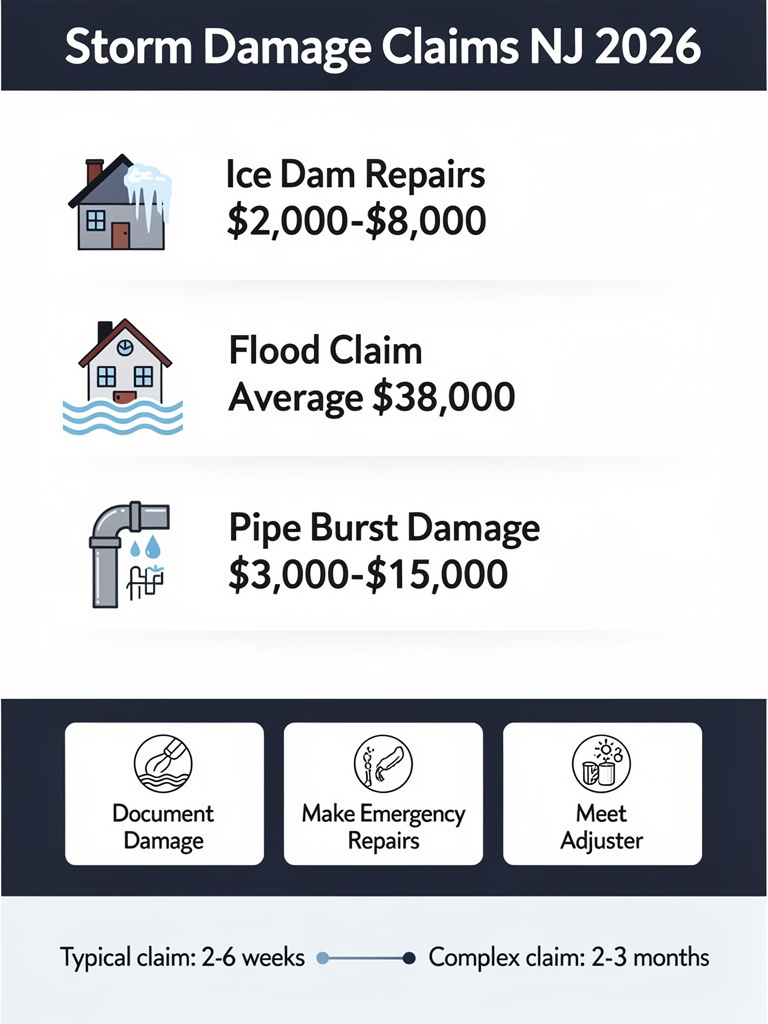

1. Stop the damage. Turn off the water main for a burst pipe. Tarp a damaged roof section. This is your responsibility as the homeowner, and most policies cover emergency mitigation costs.

2. Contact your insurance company immediately. Don’t wait. Most policies have a prompt-notification clause, and delays can complicate the claim. Get your claim number and adjuster assignment.

3. Document everything. Take photos and videos of all damage before you start any cleanup or temporary repairs. This is your evidence for the adjuster.

4. Make emergency repairs to prevent further damage. Board up broken windows, tarp the roof, and extract standing water. Keep every receipt — these costs are typically reimbursable under your policy’s loss mitigation coverage.

5. Meet with the adjuster. The insurance adjuster will visit to assess the damage. Walk through the property with them and point out every affected area.

6. Get repair estimates. Your insurer will provide an estimate, but you’re entitled to get your own. This is where hiring a handyman or contractor for an independent estimate protects you from being underpaid.

7. Complete repairs. Once the claim is approved and the settlement is issued, you can proceed with repairs. Keep all invoices and proof of completion.

When a Handyman Is the Right Call vs. a Specialty Contractor

Not every storm repair needs a roofer, a structural engineer, or a water restoration company. Here’s where the lines fall:

Call a Handyman For

- Drywall repair and replacement after water damage — cutting out wet drywall, replacing panels, taping, mudding, and painting

- Minor carpentry — replacing rotted trim, baseboards, door frames, or window casings damaged by moisture

- Gutter repair and reattachment — storm-damaged gutters that are bent, detached, or leaking at seams

- Siding repair — individual panels or sections of vinyl, aluminum, or wood siding knocked loose by wind or debris

- Interior painting after water damage repairs are complete

- Flooring removal and replacement — pulling up water-damaged carpet, LVP, or laminate subflooring

- Debris cleanup — hauling away damaged drywall, insulation, and personal property after water extraction

Any Time Any Job Handyman provides home repair services in Long Branch for post-storm damage, including drywall replacement, gutter repair, siding fixes, and painting. We’re available 24/7 for emergency storm response.

Call a Specialty Contractor For

- Major roof damage — structural roof repairs, full roof replacement, truss damage

- Foundation cracks from flooding or soil saturation

- Major plumbing — whole-house repiping, sewer line repair, water heater replacement

- Mold remediation — professional mold removal if standing water has been present for 48+ hours

- Electrical panel damage from flooding — requires a licensed electrician

The Handyman + Contractor Combo

For most moderate storm damage events, the right approach is a handyman for the interior repairs and cosmetic work, plus a specialty contractor for the heavy structural or licensed work. A handyman can also coordinate between the different trades, which saves you the project management headache.

Common Storm Damage Scenarios in Monmouth County

Winter Storms and Ice Dams

New Jersey winter storms regularly cause ice dams that force water under shingles and into attic spaces. The resulting damage — wet insulation, stained ceilings, rotted roof sheathing — is covered under most standard homeowner’s policies, as NorthJersey.com reports.

Typical repair cost: $2,000–$8,000 for ice dam damage, including roof repair, insulation replacement, and interior drywall work.

Who handles it: Roofer for the roof, handyman for the interior drywall and painting, plumber if frozen pipes are involved.

Coastal Storms and Hurricane Damage

Monmouth County’s shoreline location makes it vulnerable to coastal storms. High winds tear off shingles, rip gutters from fascia boards, and drive rain through siding seams.

Typical repair cost: [$5,000–$25,000+] for wind and rain damage, depending on severity. After Hurricane Sandy, the average flood claim in NJ exceeded $38,000.

Who handles it: Roofer and siding contractor for exterior, handyman for interior repairs, water restoration company if flooding occurs.

Frozen Pipes

When temperatures drop below 20°F for extended periods, uninsulated pipes in exterior walls, crawl spaces, and attics freeze and burst. The resulting water damage affects everything the water touches.

Typical repair cost: [$3,000–$15,000] depending on how many rooms are affected, whether mold develops, and whether the pipe itself needs replacement.

Who handles it: Plumber for the pipe, handyman for drywall, flooring, and paint restoration.

Documentation Tips That Protect Your Claim

Take photos before AND after. Before you touch anything, photograph the damage from multiple angles. After emergency repairs, photograph the temporary fixes too (tarps, boarded windows).

Keep a damage log. Write down the date, time, and circumstances of the damage. Note what you did to mitigate it and who you called.

Save every receipt. Emergency plumber, tarp purchase, hotel stay if your home is uninhabitable — all of these may be reimbursable under your policy.

Don’t throw away damaged items immediately. The adjuster may want to see them. If you must dispose of something for health reasons, photograph it first.

Get independent estimates. The insurance company’s adjuster will produce an estimate, but it’s not always comprehensive. A handyman or contractor who walks your property can identify damage the adjuster missed.

Frequently Asked Questions

1. Does homeowner’s insurance cover water damage in New Jersey?

Standard homeowner’s insurance covers sudden and accidental water damage — burst pipes, storm-driven rain through damaged roofing, and appliance failures. It does not cover gradual leaks, flood damage from rising water, or damage from deferred maintenance.

2. How do I file a water damage insurance claim in NJ?

Contact your insurance company immediately, document all damage with photos and videos, make emergency repairs to prevent further damage, keep every receipt, and meet with the adjuster to walk through the property together.

3. Does insurance cover ice dam damage?

Most standard homeowner’s policies cover water damage from ice dams if the ice dam resulted from a covered peril. The resulting interior damage, wet insulation, stained ceilings, and rotted sheathing are typically included.

4. When should I call a handyman vs. a contractor for storm damage?

Call a handyman for drywall repair, minor carpentry, gutter fixes, siding repair, interior painting, and flooring replacement. Call a specialty contractor for major roof damage, foundation cracks, mold remediation, or electrical panel damage.

5. How long does an insurance claim take to process?

Most water damage claims in NJ are processed within 2–6 weeks. Complex claims involving structural damage or disputed coverage can take 2–3 months. Emergency mitigation costs are often reimbursed within days.